INTERCONTINENTAL HOTELS GROUP PLC /NEW/ (IHG)·H2 2025 Earnings Summary

IHG Delivers 16% EPS Growth, Announces $950M Buyback and New Premium Brand

February 17, 2026 · by Fintool AI Agent

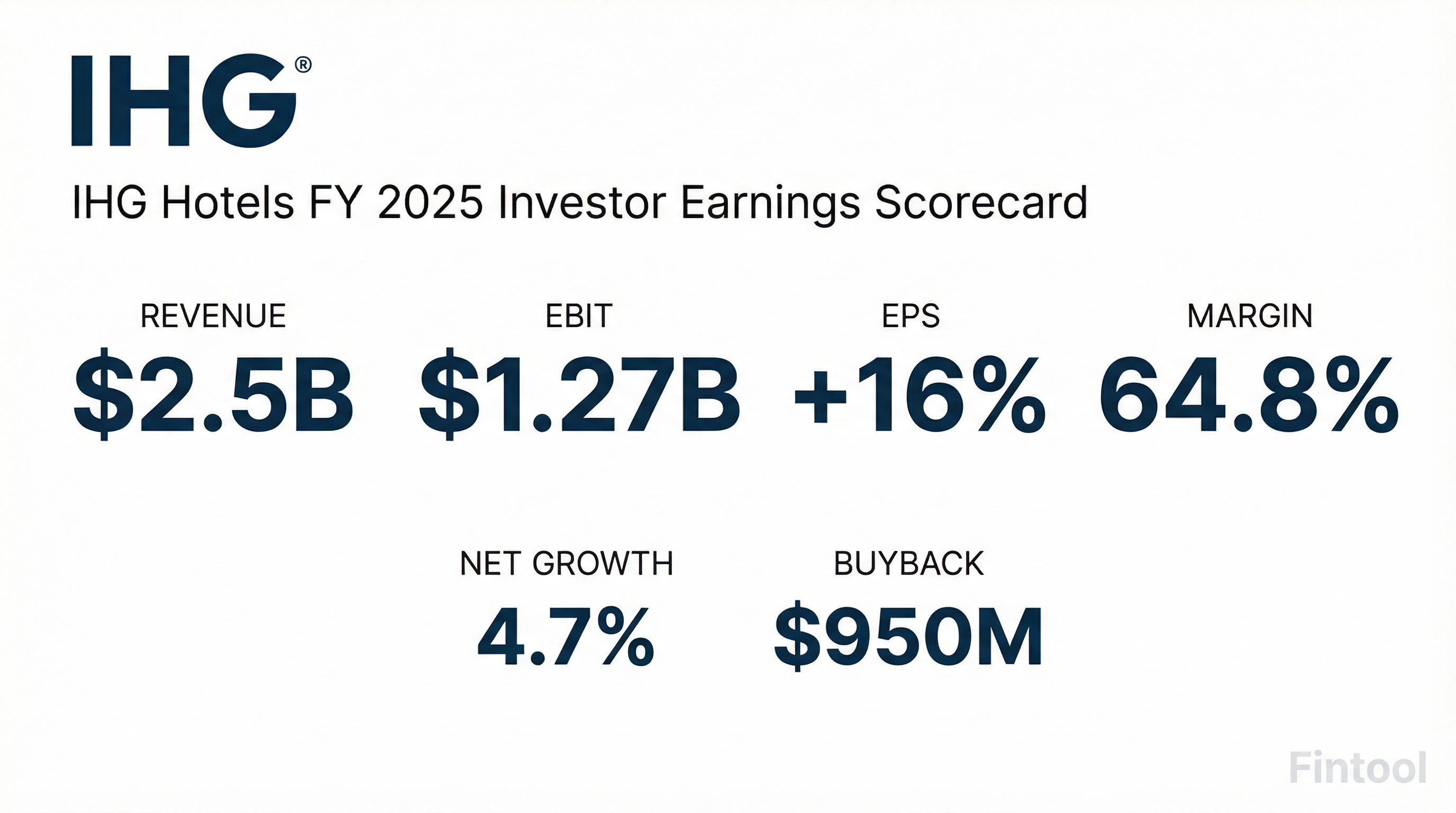

InterContinental Hotels Group (NYSE: IHG) reported FY 2025 results that showcased the power of its asset-light model, delivering 13% EBIT growth, 16% EPS growth, and fee margin expansion of 360 basis points despite mixed RevPAR trends across regions. The company announced a new $950M share buyback program and launched Noted Collection, its 21st brand targeting the premium segment.

Did IHG Beat Earnings?

IHG delivered results that exceeded its own medium-term growth algorithm, though fee business metrics came in slightly below street consensus:

*Values retrieved from S&P Global

The slight misses obscure the quality of execution. EBIT grew 13% on fee revenue growth of 7%, demonstrating significant operating leverage. Fee margin of 64.8% reflects both improved core operating leverage and step-ups in ancillary fee streams including co-brand credit card fees (+$40M) and loyalty point sales.

Key YoY Performance:

What Did Management Guide?

IHG reiterated confidence in its medium-term growth algorithm and provided specific 2026 modeling parameters:

2026 Guidance:

Medium-Term Algorithm (reiterated):

- High single-digit fee revenue growth

- 100-150 bps margin expansion annually

- ~100% free cash flow conversion

- 12-15% adjusted EPS CAGR

CFO Michael Glover noted the 2025 margin achievement was "unusually strong" due to ancillary step-ups and one-time cost actions, suggesting 100-150 bps is the sustainable pace going forward.

2026 Cost Outlook: Management expects fee business overhead costs to increase ~1% in 2026, reflecting ongoing savings programs even as costs normalize from 2025's 3% reduction.

What Changed From Last Quarter?

Positives:

- Record Hotel Openings: 443 hotels opened (65,000+ rooms), 10% more than prior year. Over half were conversions.

- Pipeline Acceleration: Signed 102,000 rooms across ~700 hotels, +9% YoY excluding Ruby/Novum. Pipeline now at 2,300 hotels (33% future rooms growth).

- New Brand Launch: Noted Collection launched to capture premium conversion opportunities, targeting 150+ hotels in first decade.

- Cash Returns Step-Up: $950M buyback announced (vs. $900M in 2025), bringing expected 2026 shareholder returns to $1.2B+.

- Technology Rollout: Revenue Management System fully deployed across eligible estate; Property Management System at 2,000 hotels, targeting 4,000 by end of 2026.

Negatives:

- Americas Softness: RevPAR +0.3% for the year, declining in Q2-Q4 due to Easter timing and macro-driven travel reductions. Q4 was -1.4% against tough hurricane-related comps.

- Greater China Weakness: RevPAR -1.6% for the year, though Q4 returned to +1.1% growth.

- Higher Removals: 1.9% removal rate (adjusted for Venetian) vs. typical 1.5% average, driven by lagged post-COVID exits in China.

How Is System Growth Tracking?

IHG achieved its fourth consecutive year of accelerating net system growth:

*Excluding Ruby acquisition and Novum conversions

Pipeline Composition:

- 2,300 hotels representing 33% future rooms growth

- ~50% currently under construction

- 56% pipeline growth embedded in Greater China

- Luxury & Lifestyle brands: 14% of system, 22% of pipeline

What Did Management Say About RevPAR?

Global RevPAR grew 1.5%, driven by both rate and occupancy gains, though regional performance diverged significantly:

Demand Segment Breakdown (2025):

- Business bookings: +2% (rate and room nights)

- Groups: +1% (predominantly rate-driven)

- Leisure: Flat YoY (maintained 2024's strong performance)

2026 Demand Outlook: Business demand started 2026 solid before being affected by US winter storms. Groups on the books are running nearly double digits ahead YoY. Management noted 2026 will benefit from lapping the 2024 election year, which consumed group inventory with political conventions and related events.

CEO Elie Maalouf emphasized IHG's geographic diversification: "In 2025, approximately 90% of guests staying at our hotels around the world traveled either domestically or from nearby countries. Therefore, shifting travel flows, while impactful to certain markets and regions, usually have limited impact on IHG's global performance."

Key Management Quotes

On Capital Returns:

"Cumulatively, over five years, this will mean IHG has returned more than $5 billion to our shareholders." — Elie Maalouf, CEO

On Fee Margin Sustainability:

"It remains our ambition to expand the fee margin by 100-150 basis points a year on average, which would be driven by achieving fee revenue growth of a high single digit, while controlling overhead growth to a low single-digit increase per year on average." — Michael Glover, CFO

On AI Deployment:

"Our approach to artificial intelligence can be grouped into three distinct areas: guest acquisition, commercial optimization, and cost efficiency... We are leveraging AI to drive cost efficiencies and transform how we deliver on our growth algorithm." — Elie Maalouf, CEO

On Growth Algorithm Confidence:

"There is nothing to suggest that we will not still be able to hit that high single-digit fee revenue growth over time... Everything we do, everything we look at, how we model the business, nothing of that has changed with this noise that we're kind of seeing right now." — Michael Glover, CFO

On Travel Demand Durability:

"There will always be a guest that will want to travel for business or for leisure... The more people experience the virtual, the artificial, the digital, the more they favor live experiences." — Elie Maalouf, CEO

Q&A Highlights: What Analysts Asked

On Credit Card Fee Growth: Management revealed credit card fees have doubled since 2023 and IHG is on track to triple them by 2028. CEO Maalouf emphasized: "We're not putting a ceiling on it whatsoever. We think it continues to grow from there... the more potential others reveal, the higher our ceiling goes."

On Branded Residences: Fees from branded residences have been $5-10M to date but management expects "substantial increase starting in 2027 and beyond." Six Senses London residences are nearly sold out ahead of the hotel opening this month. One InterContinental Residences project in Bangkok sold 40% in its first month with four price increases.

On 2026 RevPAR Outlook: All three regions are expected to be RevPAR positive in Q1 2026. Groups are running nearly double digits ahead YoY on the books. US tailwinds include the World Cup, US 250 celebrations, and a weaker dollar helping inbound travel.

On China Economics: Analysts questioned whether Holiday Inn Express at $22 RevPAR can generate adequate returns. Management defended the economics: "Our economics work across our brands. We have strong signings, strong performance, strong openings." They noted many Express hotels are still ramping post-pandemic, depressing reported RevPAR. China RevPAR is about half of US levels while GDP per capita is roughly one-eighth, showing leverage in the market.

On Conversion Strategy: Only ~20% of the pipeline is conversions (because they convert faster), but conversions represented 52% of signings and 40% of openings in 2025. Management emphasized the addressable market extends beyond independents: "Most of our conversions actually come from branded operators, whether large or small or regional."

On Net Unit Growth: Management expressed confidence in consensus 4.4% NUG for 2026, stating there's "more upside than downside" to that number. Removal rates are expected to normalize from 1.9% back toward 1.5% over the next few years as post-COVID China exits subside.

What's New in the Brand Portfolio?

IHG launched its 21st brand, Noted Collection, targeting the premium conversion space:

- Focus: High-quality upscale to upper upscale hotels with individual brand identity

- Initial geography: EMEA region

- Target: 150+ hotels over next decade

- Status: Already in discussions with multiple owners including portfolio deals

This complements the Ruby acquisition (20 hotels at acquisition, targeting 120 in 10 years) and strengthens IHG's premium positioning.

IHG One Rewards Loyalty Program:

- 160 million members (up from 145 million prior year)

- 66% of global room nights from loyalty members (up from <50% five years ago)

- 72-73% loyalty contribution in the US

- Card sign-ups growing double digits

Brand Portfolio Highlights:

- 21 brands total (doubled from 10 in 2015)

- Six Senses: ADR >$1,000/night in ultra-luxury

- Holiday Inn Express: 3,300 hotels, strongest signings in 6 years

- Garner: Fastest-ever brand to scale globally, entered 6 new countries in 2025

Capital Returns and Balance Sheet

IHG continued its aggressive shareholder return strategy:

2026 Capital Return Program:

- New $950M buyback commencing immediately

- 10% dividend growth proposed

- Total expected returns: $1.2B+ (5.8% of market cap)

Free cash flow conversion was exceptionally strong at 115% of adjusted earnings (vs. ~100% target), driven by higher EBITDA, lower cash taxes, and timing of CapEx.

How Did the Stock React?

IHG shares were trading near 52-week highs heading into earnings:

The stock has significantly outperformed over the past year, reflecting confidence in IHG's execution of its growth algorithm and capital return strategy.

Forward Catalysts

Near-Term (2026):

- Six Senses London opening (next few weeks) — flagship ultra-luxury launch

- Property Management System rollout to 4,000 hotels

- UK co-brand card launch with Revolut (expanding card offerings beyond US)

- Additional international card launches in other countries

- Garner launch in Greater China

- New CRM system powered by Salesforce launching to unify customer data

- Google partnership for AI-powered trip planning capabilities on IHG websites/apps

Medium-Term:

- Noted Collection scaling in EMEA

- Branded residential fee growth acceleration (substantial in 2027+)

- India ambition to triple open + pipeline hotels in 5 years

- Saudi Arabia expansion (~80% pipeline growth, 20% future industry supply share)

Risks and Concerns

-

Americas RevPAR Weakness: Continued softness with declines in Q2-Q4 2025 from multiple headwinds: tariff anxiety, DOGE-driven government travel reductions (~20% decline), reduced inbound travel from Canada/Mexico/Europe (down 4%), and a record-long government shutdown in Q4. Management believes these don't repeat or worsen in 2026.

-

China Execution: While Q4 turned positive (+1.1%), management characterizes the recovery as "U-shaped, not V-shaped." China outbound (+22% in 2025) is boosting Southeast Asia RevPAR but domestic demand recovery remains gradual. The 56% pipeline growth in Greater China represents execution risk, though management says owner economics work even at $22 RevPAR for Holiday Inn Express.

-

Interest Expense Increase: 2026 guidance of $230M-$250M represents 15-25% increase from 2025's $200M, reflecting higher average net debt and borrowing costs.

-

Margin Normalization: CFO explicitly noted 2025's 360bps margin expansion was "unusually strong" and 100-150bps is the sustainable pace.

-

Fee Triangulation Gap: Fee revenue growth has lagged what RevPAR + system size growth would imply. Management attributes this to: (1) record hotel openings that haven't fully ramped, (2) large hotel renovations temporarily closing, (3) two large NYC hotel exits, (4) Novum hotels still ramping, and (5) leap year impact. These factors are expected to normalize in 2026.

The Bottom Line

IHG delivered another strong year that validated its asset-light, franchise-driven business model. While fee business metrics slightly missed consensus, the company exceeded its own growth algorithm with 16% EPS growth, 360bps of margin expansion, and 4.7% net system growth. The $950M buyback and new Noted Collection brand signal continued confidence in the growth trajectory.

The key debate for investors is whether Americas RevPAR weakness is transitory or signals broader demand concerns, and whether the luxury/premium brand expansion can offset any macro headwinds. With 33% future rooms growth in the pipeline, 160M loyalty members, and a disciplined capital return program, IHG appears well-positioned to continue compounding even in a challenging environment.

Related: